Top Mortgage Lenders in Albuquerque NM for Retirees

Top mortgage lenders in Albuquerque NM for retirees: rates comparison, reviews, and the best options for downsize buyers

The best mortgage lenders for Albuquerque retirees are those that verify retirement income flexibly, offer rate and fee transparency, and provide senior friendly programs like low cost options, buydowns, and reverse mortgage expertise. You should anchor your lender search to your retirement income profile, your time horizon in the home, and your cash from the sale of your current property (selling your current home and buying in Albuquerque NM as a retiree

Why This Matters Right Now

You are shopping in a buyer friendly Albuquerque market with more inventory and a steady pace of sales. That gives you leverage on price and closing costs, but financing still drives your total cost and monthly comfort. With 30 year rates hovering near the mid to high 6s and 15 year options a bit lower based on recent national indicators, your lender choice can mean tens of thousands in lifetime savings. As a retiree, you also face unique underwriting issues, like documenting Social Security, pensions, and assets. Your timing could let you secure a better payment, negotiate lender credits, and choose a product that fits how long you plan to stay. Pick the right lender now and you will downsize with confidence, fewer surprises, and a monthly budget that fits your retirement plan.

What You Need to Know Before You Choose a Lender

You should anchor your lender search to your retirement income profile, your time horizon in the home, and your cash from the sale of your current property. Lenders evaluate you differently in retirement, and the best ones in Albuquerque know how to use every eligible guideline to your advantage.

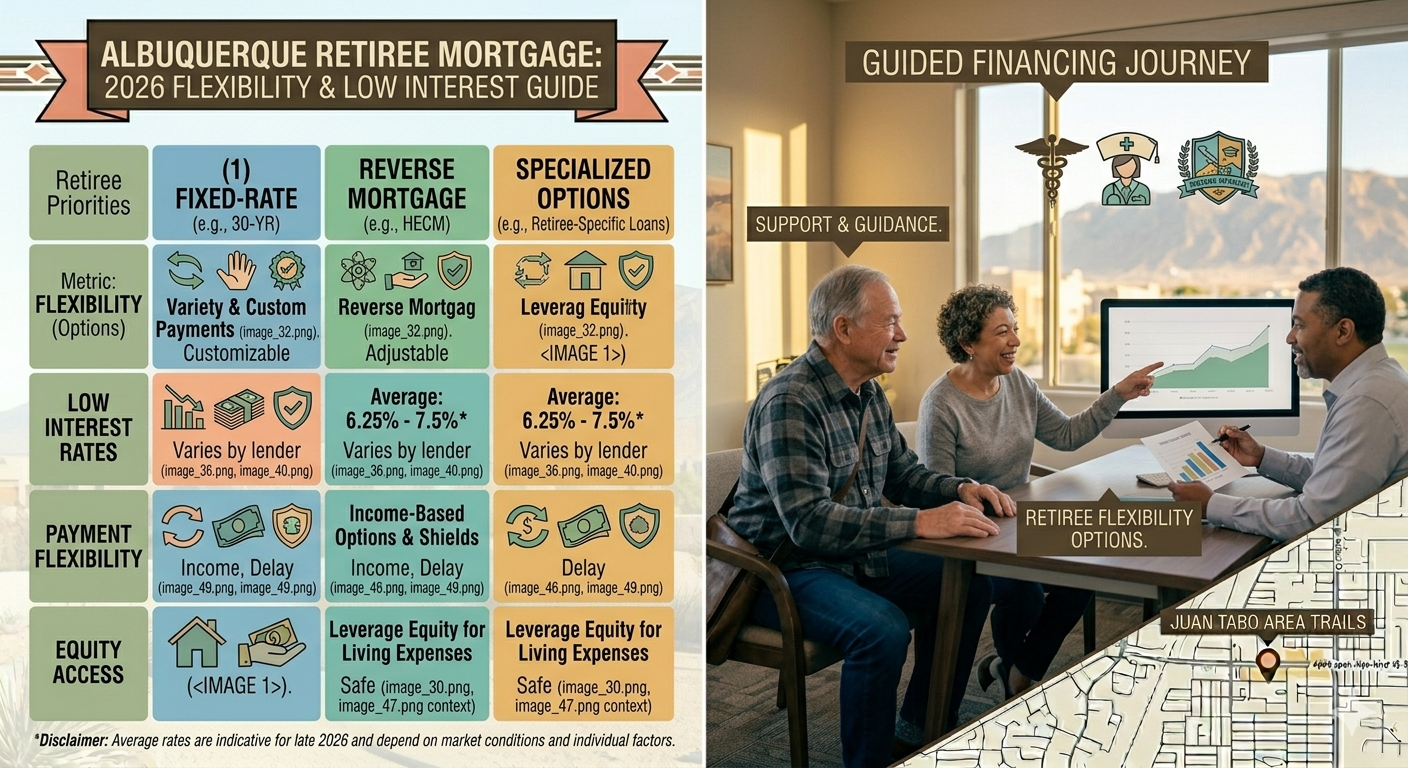

- Income matters even if you do not draw a paycheck. You can qualify with Social Security, pensions, annuities, required minimum distributions, and sometimes asset depletion. Good lenders help you structure this cleanly.

- You have product choices that fit downsizing. Options include 30 year fixed, 15 year fixed, adjustable loans if you plan a shorter hold, HELOCs to bridge the gap before your current home sells, and HECM for Purchase if you want a reverse mortgage with no monthly principal and interest payment.

- Rates shift daily. National benchmarks from FRED and Freddie Mac show 30 year fixed rates in the mid to high 6s and 15 year fixed in the low to mid 6s recently, but your final rate depends on credit score, loan to value, property type, and discount points. Confirm current conforming limits before you lock in a product (Fannie Mae Loan Limits and FHFA 2026 Loan Limits)

- Upfront costs can be negotiated. In a buyer friendly market, you can often trade a small price concession for sizable lender or seller credits that cover title, escrow, or a rate buydown.

- Taxes and fees are part of the payment. Bernalillo County offers a Senior Property Tax Exemption on a portion of assessed value for eligible homeowners 65 and older, which can trim your escrowed tax amount. Factor HOA dues carefully if you prefer low maintenance living.

Local lenders that regularly serve retirees in Albuquerque include credit unions with member focused pricing and mortgage brokers who shop multiple investors. Reverse mortgage specialists can be valuable if you want to preserve monthly cash flow. You should verify licensing, ask for a written cost worksheet, and confirm turn times for appraisal and underwriting before you commit.

A quick rates snapshot

- 30 year fixed purchase with good credit: often in the 6.75 to 7.00 range with zero points, lower if you pay points.

- 15 year fixed: often 0.25 to 0.50 lower than 30 year, with higher required payment but faster equity build.

- HELOCs: variable and tied to a benchmark index. Best if you need short term access to equity.

- Reverse mortgages: a different rate structure and upfront insurance. Best if you want no monthly principal and interest payment and plan to age in place.

How to Compare Your Options

You will get the best result by comparing lenders on total cost, underwriting flexibility with retirement income, and service speed. Aim for at least three written quotes on the same day with the same assumptions.

- Compare APR, not just rate. APR reflects points and most fees. A slightly higher rate with low fees can beat a teaser rate with heavy points if you plan a shorter hold.

- Match the loan term to your horizon. If you plan to stay 5 to 7 years, a lower cost option or even a conservative adjustable may outperform a 30 year fixed. If you plan to age in place, a 30 year or HECM for Purchase could fit better.

- Evaluate how the lender handles senior income. Ask how they gross up nontaxable Social Security, how they document pension continuance, whether they allow asset depletion calculations, and what they need for trust or annuity income.

- Confirm rate lock options. You should know lock length, extension fees, and whether a one time float down is available if rates drop before closing.

- Ask about credits and buydowns. Lender paid credits can offset closing costs. Temporary buydowns like 2 1 can cut your payment in years one and two if that helps with early retirement budgeting.

- Check service and communication. You want a dedicated loan officer, proactive milestone updates, and a clear list of documents upfront to avoid last minute stress.

- Look at local appraisal turn times. Albuquerque appraisals usually move quickly, but a lender with reliable local appraisers reduces delays. For guidance on inspections and what to expect from property exams, review how to choose the best home inspectors in Albuquerque NM for relocating buyers

Key factors to evaluate:

- Underwriting approach to retirement income and assets, especially Social Security and RMDs

- Total cost over your expected holding period, not just the upfront rate

- Lock strategy, credits, and buydown availability in a buyer friendly market

Your Step by Step Guide

1) Clarify your budget. Decide your target monthly outlay for principal, interest, taxes, insurance, and HOA. Keep this at or below 30 percent of your retirement income for comfort.

2) Gather documents. Collect Social Security award letters, pension statements, two years of 1099s, recent bank and investment account statements, and any trust documents. If you will sell a home, prepare your estimated settlement statement.

3) Choose your path. Decide among a traditional mortgage, a HELOC bridge, or a HECM for Purchase if you want no monthly principal and interest payment. Align this with how long you plan to stay.

4) Request three same day quotes. Ask for a standardized cost estimate with rate, points, lender fees, third party fees, and an estimated escrow. Keep assumptions the same so you can compare apples to apples.

5) Stress test the payment. Model taxes, insurance, and HOA increases. If you might pay off the loan early or recast after your sale, ask the lender to show that scenario.

6) Lock your rate. Once you have a purchase agreement, lock for a realistic period based on appraisal and underwriting turn times. Clarify extension terms and float down options.

7) Appraisal and title. Your lender orders the appraisal and title work. Ask for regular updates, especially if the property has unique features like solar or an ADU.

8) Final conditions. Respond quickly to any underwriting requests. If you plan to use asset depletion or RMDs, confirm exactly how withdrawals must be documented.

9) Closing review. Request a closing disclosure at least three days in advance. Verify the rate, cash to close, and that any negotiated credits appear correctly.

10) Post close plan. Set up automatic payments, consider a recast after your current home sells if you used a low down payment, and schedule your homestead and senior tax exemptions if eligible.

What This Looks Like in Albuquerque NE Heights, West Side, and North Valley

You will see different property profiles by neighborhood, which should influence your loan choice. Around the Juan Tabo and Northeast Heights area, you will find established neighborhoods with mature trees, close access to the Sandia Mountains, and a mix of classic ranch and updated single story homes. Average prices tend to run near the upper three hundreds to low four hundreds in many subdivisions. If you want walkability and low yard work, you will likely see HOAs, so factor those dues into your payment.

On the West Side, you will find newer single story floor plans and good value for money in the mid three hundreds. If you plan a shorter hold or expect to sell within seven years, a lower cost loan or a 15 year option could build equity faster without a big price tag. Summer heat and sprawl mean you should check utility estimates and drive times to healthcare.

In the North Valley, you will find larger lots, casitas, and quiet ditch trails. Prices often land around the mid three hundreds, with opportunities to add an accessory dwelling unit. If rental income from a casita will help your retirement plan, ask your lender whether it can count for qualifying. Appraisal complexity can be slightly higher due to lot size and property uniqueness, so choose a lender with reliable local appraisers.

Neighborhoods to consider: top neighborhoods in Albuquerque

- Northeast Heights: Strong single story inventory near trails and shopping, roughly upper three hundreds to low four hundreds, low crime pockets and mature landscaping

- West Side: Newer builds with modern layouts in the mid three hundreds, convenient highway access and schools

- North Valley: Rural feel with orchards and ADU potential around the mid three hundreds, serene setting near the bosque

What Most People Get Wrong

You might assume the lowest advertised rate is your best deal. In practice, the lowest rate often carries steep points that take many years to break even. If you plan to sell within seven to ten years, you usually come out ahead with a slightly higher rate and lower upfront costs.

You might also think your retirement income limits your options. Lenders experienced with retirees can gross up nontaxable income and use responsible asset depletion to help you qualify safely. Another common miss is overlooking the HECM for Purchase. If you want to preserve monthly cash flow, a reverse mortgage purchase can be a smart way to buy with a large down payment and no monthly principal and interest payment, as long as you understand insurance costs and long term obligations.

Finally, you might ignore taxes and HOA dues until late in the process. Your payment comfort depends on the full PITI plus HOA, so model those early and capture any senior tax exemptions you qualify for.

Frequently Asked Questions

Who are the top mortgage lenders in Albuquerque for retirees?

You have strong choices among local credit unions, independent mortgage brokers, and reverse mortgage specialists. Credit unions often price competitively for members and understand local appraisals. Brokers shop multiple investors for you. Reverse specialists are best if you want a HECM for Purchase.

What rates should you expect right now in Albuquerque?

You should expect 30 year fixed rates in the mid to high 6s and 15 year fixed in the low to mid 6s, based on recent national indicators. Your exact rate depends on credit score, down payment, points, and property type. Always compare APR and total cost over your expected holding period.

Are reverse mortgages a good option for downsizing?

They can be, if you want no monthly principal and interest payment and plan to age in place. A HECM for Purchase lets you buy with a large down payment and finance the rest with a reverse mortgage. You must occupy the home, pay taxes and insurance, and maintain the property. Review costs and inheritance goals carefully.

How do you qualify for a mortgage if you are retired?

You qualify with documented retirement income like Social Security and pensions, plus assets. Lenders may gross up nontaxable income and can use asset depletion. Provide award letters, 1099s, and statements for bank and investment accounts. A seasoned loan officer will guide you through documentation.

Which local programs help Albuquerque retirees lower housing costs?

You can apply for Bernalillo County’s Senior Property Tax Exemption if you are eligible. Some lenders offer small rate discounts for borrowers over 62, plus lender credits and buydowns that cut early payments. If you are a veteran, a VA loan with no down payment and possible funding fee relief could be your best path.

The Bottom Line

You will get the best downsizing result in Albuquerque by pairing a buyer friendly market with a lender that understands retirees. Compare three same day quotes, focus on APR and total cost, and choose a product that fits your time horizon. Credit unions, strong local brokers, and reverse mortgage specialists can all be excellent, as long as they document your retirement income cleanly, move quickly on appraisal and underwriting, and offer clear rate lock and credit options. When you align product, payment, and neighborhood, you will downsize with confidence and keep your retirement plan on track.

If you are ready to explore your options for top mortgage lenders in Albuquerque and the best fit for your downsizing plan, Vinay Rodgers at The Rodgers Neighborhood Real Estate Group can walk you through the specifics for your situation (meet Jenn and Vinay your trusted New Mexico realtors

5054172733

5054172733

Categories

- All Blogs (260)

- 2026 & Beyond for Real Estate (158)

- Doctors and Nurses looking for homes in NM (4)

- Guide to buying a home in NM (122)

- Health Care Heros (6)

- Home Upgrades (25)

- Jenn & Vinay your Local Real Estate Experts! (86)

- Moving to Albuquerque (97)

- Neighborhoods in Albuquerque NM (73)

- Rent or Own (2)

- Sellers Questions for Selling homes (2)

Recent Posts

GET MORE INFORMATION